By Mark Pruner

The May Greenwich Real Estate Report

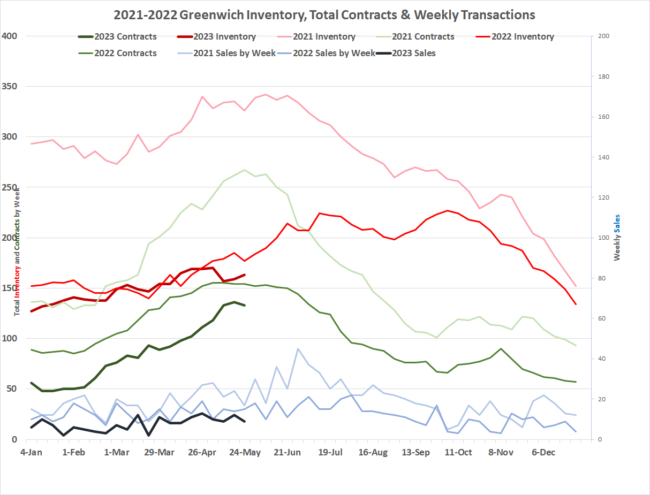

Four years ago, at the beginning of June 2019, we had 738 single family homes on the Greenwich MLS. This year at the beginning of June, we have 164 houses listed. Think about that, we had 584 more houses on the market four years ago than we have now. That’s a drop of 78% and the drop of 584 listing is not that far from the total of 624 houses we sold for all last year.

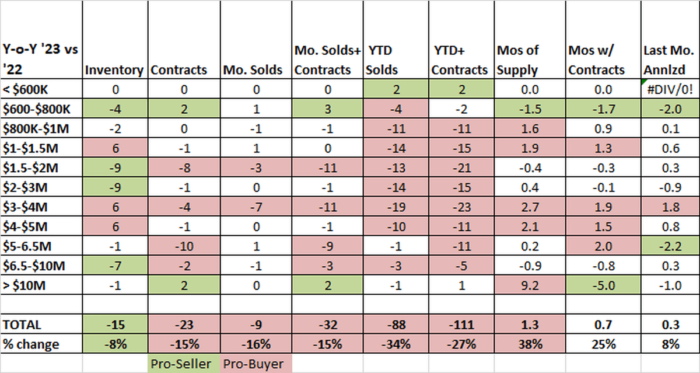

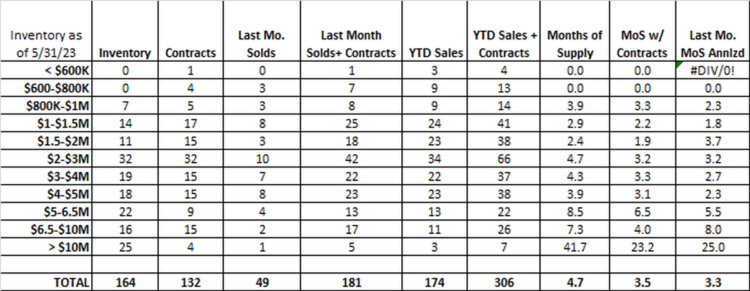

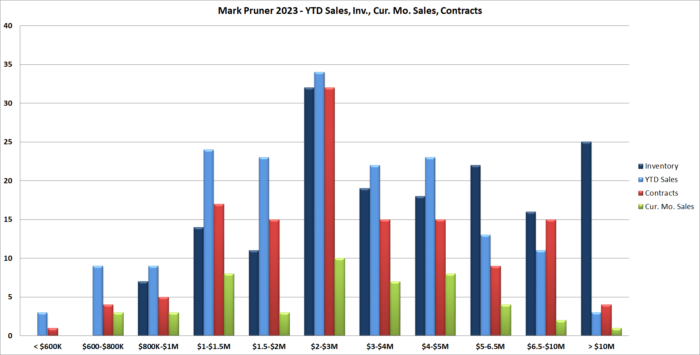

To show how low inventory is, let’s look at some factoids. We have no listings under $800,000. Under $1,000,000 we only have 7 listings. Of those 7 listings only 2 have been on for more than 50 days. In Riverside we only have 10 listings and of those 10 listings only 1 listing is under $2.2 million. It’s a tight market.

For much of this year, our inventory levels tracked last year’s inventory levels, however, that changed in May. Every week in May 2023 was a new all-time low for inventory each week. This drop in inventory is due to both fewer new listings and fewer contracts, i.e., less supply and less demand. At the present time, we have 132 contracts waiting to close compared to 154 contracts last year at this time.

Higher interest rates and anemic stock and bond markets are clearly hurting sales, but a lack of new listings is an equal, if not greater factor, in our sales being down 34% from last year. Last year for the first five months we had 407 new house listings. This year we have only had 340 new listings or a drop of 16.4%. Arguably, half of our 34% drop in sales is from fewer listings coming on and the other half of the drop in sales is from less demand. That, however, is very uncertain as both the median days on market and sales price to original list price ratio are showing a slightly tighter market.

The common wisdom is that sellers are locked into their present houses by a decade of artificially low mortgage rates kept that way by the Fed. That’s a decent argument up to $2 million as many buyers in this price range do use bank financing. In Greenwich, however,

I think that is a minor part of the market dislocations that we are seeing.

Most of our buyers don’t use mortgage financing and the higher you go in price the less mortgage financing you see. Above $4 million, you do see people buying higher priced houses with low-rate mortgages, to free up cash for other investments. In 2018, the incentive to use mortgage financing was reduced somewhat as mortgage deductibility was limited to $750,000, down from $1.1 million that was allowed in prior years.

In addition, many of our sellers are downsizers, who paid off their mortgages decades ago. Lower interest rates are not holding them captive as they are not paying any interest. Most of these downsizers are also sitting on large increases in equity in the hundreds of thousands, and even millions, of dollars. They are most likely going to be buying their next home with all cash as it is usually a smaller house or condo, and they have plenty of cash for that purchase. “Higher” interest rates don’t scare these seniors as they lived through mortgage rates in the 1980’s that went as high as 17%, so just how scary is a 6% mortgage rate. Of course, few of them are actually going to have to pay today’s rates, since the purchase of their new, smaller unit is likely to be all cash.

In Greenwich much of our lower inventory is due to gridlock. Many people who would like to buy a house can’t find anything to buy. As a result, they stay in their homes resulting in a dark spiral of lower inventory, leading to lower inventory. Many pundits see this period of lower inventory lasting for a year, two years, or even more.

Will we ever see higher inventory levels? The answer to that is “of course”, it’s just a matter of when. We may actually see a rise in inventory faster than many expect. To see how this might happen look at the Yukon River.

Each year Dawson City, Alaska has a contest to pick that data that the ice will break-up on the Yukon River. It happens quickly when it does. As the first ice is able to move it opens up pathways for the ice behind it, leading to a quick change from icebound to open water. Our market could be like that. As more houses finally come on, more buyers can buy. These buyers then put their own houses on the market, meaning more people can buy. It won’t happen as fast as the Yukon River breakup, but once it starts, we could see things change in few quarters, not a few years.

Increased inventory, whether taking many months or few years, may only moderate prices. Right now, we need a lot more inventory to meet our present demand. Our market is actually slightly tighter than last year. Our days on market is down this year and the sales price to original list price is up. The median sales price for 2023 is $2,560,000 up 1.4% from last year’s $2,525,000. None of these are big changes, but at the present time, and until the log jam is broken, our supply, all the way up to $5 million, is not meeting our demand.

This is not to say that every house is jumping off the market. Of our 164 listings, 53 have been on for more than 6 months and 23 of them have been on for more than a year. Older houses that need work and don’t have today’s more open floorplan can be a tough sale. On the flipside, something that is new, or has been recently renovated, usually sells quickly with multiple all-cash offers. Having said that, even in this market you can put too high a price on a house. Of the 53 houses that have been on for more than six months, 14 were built in the last three years.

Right now, inventory is plumbing new lows, but babies are being born, people are getting married, (or divorced), getting new jobs or changing jobs and more inventory will come, it’s just not clear when, but it’s not going to be next month.

Stay tuned . . .

Mark Pruner is a Realtor with Compass. He can be reached at 203-817-2871 or mark.pruner@compass.com