By Mark Pruner

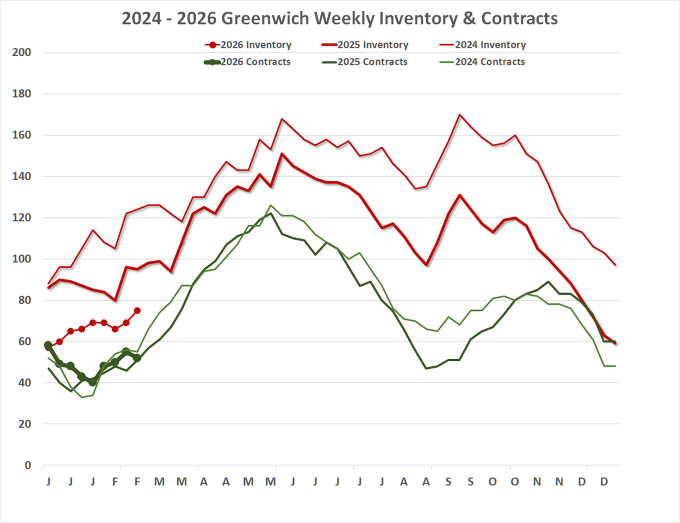

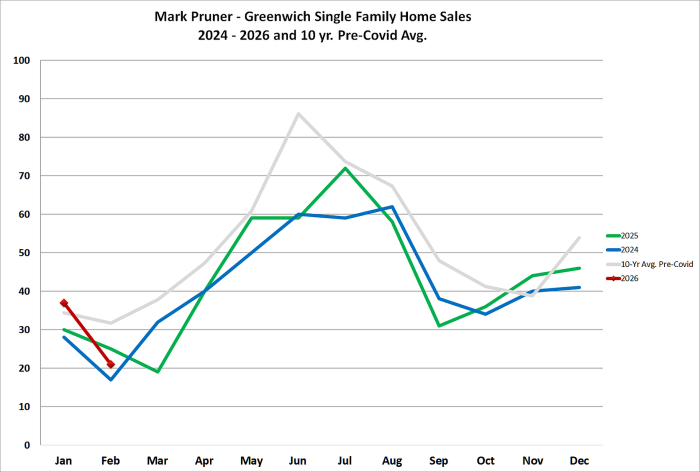

How much do two major snowstorms and a near record extended cold period affect sales? The answer is a good deal. We saw above average sales in January 2026 as we carried over 58 contracts from the end of December 2025. By the end of January, many of these contracts had closed. We added some 28 contracts in February, but with sales and we were down to 41 contracts by the end of January. This big drop in contracts pushed January 2026 sales above our 10-year preCovid average.

Our 37 January sales looked like good news, and it was for those reports that missed that our contracts had taken a nosedive. Then came February and weeks of cold weather and a lot of snow. This kept inventory off the market. Yes, inventory went up in January and February, but it was starting from record low levels. What the snow and cold caused was a drop in people listing their houses in a market that had motivated buyers.

For many buyers their motivation couldn’t overcome blizzards and snow up to your knees. Our sales in February dropped to only 21 sales, compared to 25 sales in February 2025. A small drop but a big drop from our 10-year average sales of 32 February The result was that our February 2026 sales were down 34%.

Despite the drop in sales, our contracts actually eked up 2 from 50 contracts last year to 52 contracts this year. This was because those brave buyers who did venture into the snow were really motivated. You can see this when you look at our days on market for contracts signed in February. The average was only 47 days on market. In January, we saw 147 DOM for January deals. Not only were there fewer, but more motivated, buyers; these buyers had the cash.

Whither the mortgage contingency

The mortgage contingency deal has almost disappeared. Of our 52 contracts at the end of this February, only 5 of them had a contingency, not even 10% of our outstanding contracts. To be fair, 16 of the remaining 47 pending contracts had previously had a contingency. But at least half of those 16 prior contingent contracts likely weren’t mortgage contingencies. As the contingencies were either removed in days or not for several months.

When I was a real estate attorney, back in the 90’s the standard mortgage contingency was for 45 days. This was because the unhurried buyer, often hadn’t even talked to their banker, or even chosen a banker, until the contract was signed. They need a month and a half to fill out the paperwork, answer the innumerable questions that came back and actually get a mortgage commitment letter.

This is not the case today. Lots of mortgage contingencies are down to 30 days. Not only are they a third shorter, but today’s prepared buyers are removing mortgage 30-day mortgage contingencies in 21, or even 14 days. These buyers are doing this because they know that the majority of competing buyers, they are going up against have the cash or are underwritten pre-approved for a loan.

This means that the buyer has worked with their banker to fill out every form, provide all of their background information and responded to every query their banks underwriting department has made. The bank only needs to see a signed house purchase contract and a house appraisal to do the deal. The time for getting these two things completed is more like 14 days.

Smart agents are also pushing their buyers to keep the contingency period as short as possible. Previously, if a buyer had a signed contract with a mortgage contingency, they were in the driver’s seat. The buyer could decide to exercise the contingency and terminate the contract and get all of their deposit back or waive the contingency and close the deal. All this time, the seller was bound while waiting for the buyer to decide whether they wanted to go forward or not.

Today, it’s not so clear cut. Our inventory is so low, that we are seeing more buyer’s and agents asking to see listings that are under a contingent contract. Then if this new potential buyer likes the house, they will put in a higher back-up offer. This ups the pressure on the previous buyer that is under contingent contract. The buyer can still ask for a mortgage contingency extension, but they may not get it, given the seller can make more money going with the back-up offer. The seller gets back some power.

We are even hearing of highly motivated second buyers offering to pay the second buyer a go-away fee. It’s not common, but it’s something that we now discuss with second buyers in this lowest-inventory market ever.

How tight is the market?

For the full market, we are looking at only 3.6 months of supply. From $1-1.5 million we have 0.9 months of supply. Only over $5 million, do we have more than 4 months of supply. Even above $5 million, we have record low MoS, with 4.3 MoS from $5-6.5 million and 6.4 MoS over $10 million. Throw in the 6 contracts that we have pending over $10 million and the ultra-high-end months of supply drops to 5.1 months of supply. One of the lowest we have ever seen for the high-end of the market.

The good thing is that while we have little inventory, it is spread out throughout the town as are the contracts. The hot areas as usual are in Old Greenwich south of the village and central Greenwich. In OGSOV, you have two choices at $4.5 million and $6.25 million. In downtown Greenwich, you have three choices: two from $3-4 million and one at $7.7 million. We also have another 25% or so private listings spread throughout the town. Even with that it’s still a very tight market.

I’m hoping that while sales and inventory are well below normal, that once we get rid of this snow, we will have a release of snow-delayed inventory. And even more buyers getting out and making deals.

Stay tuned…

Mark Pruner is a co-founder of the Greenwich Streets Team at Compass. He can be reached at 203-817-2871 or mark.pruner@compass.com.