By Mark Pruner

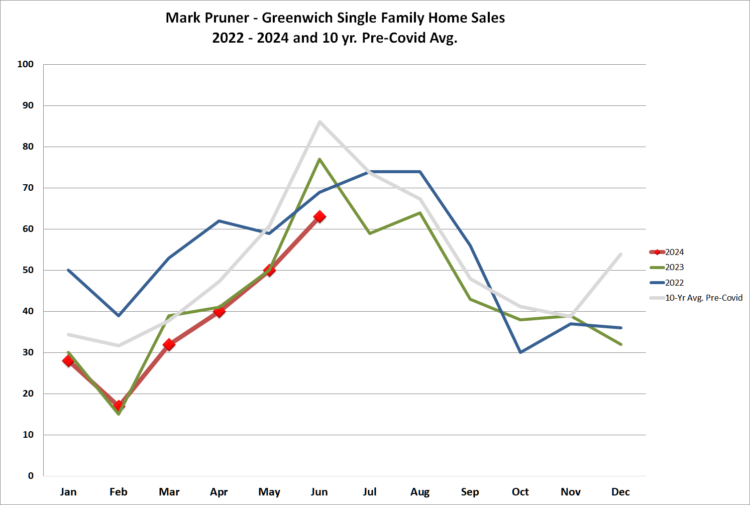

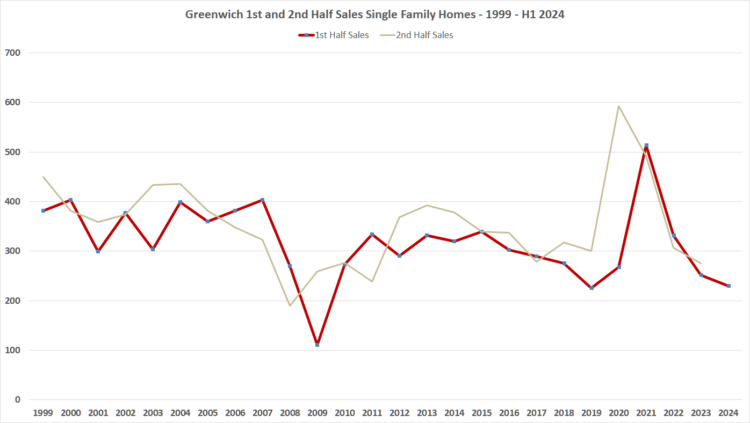

So, what’s going to happen in the second half of 2024? If you take a look at history of the last 25 years, our second half sales are about 10% higher than the first half. Since our first half sales were only 230 sales, that would tend to indicate that we would end 2024 with about 483 sales. This means that we would have to go all the way back to the Great Recession year of 2009 to find a lower annual sales number.

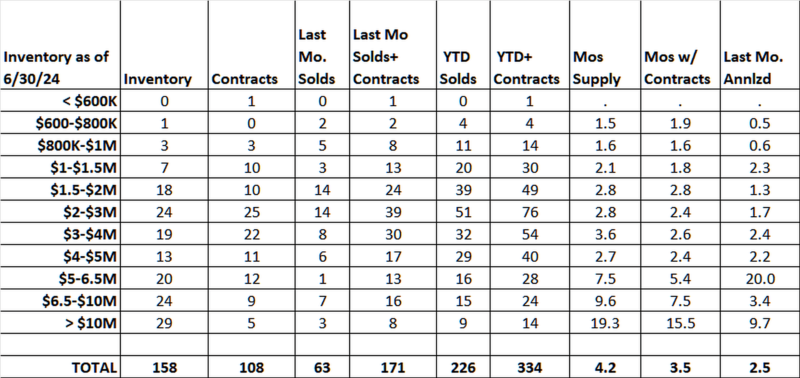

If, however, we go back to the last three years, then the second half numbers are pretty similar to the first half numbers, which means that we would be looking at an even lower number of annualized sales at 460 sales. Now add in the fact that our inventory is 158 single family homes, up only slightly from the very low inventory of 146 houses that we had at the end of the first half of 2023; and our market is looking pretty bleak.

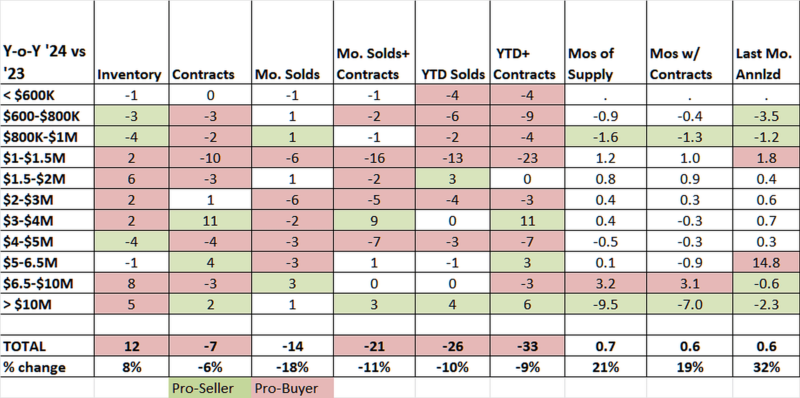

On the other hand, you can also argue that we are in a very hot market for the inventory that we do have. While our house inventory is up 8% over what we had in 2023 at this time; we are still down 78% from the inventory that we had at this time in 2019.

Just about every other indicator shows that 2024 is a tighter and more pro-seller market than we had last year:

• Our median sales price is up from $2.55 million last year to $2.73 million this year or an increase of 7.1%

• Our days on market is down from last year’s very low 33 days on market to an even lower 21 days on market, i.e., last year the median house took just over a month to get to a non-contingent contract. This year it only takes three week.

• Our median sales price to assessment ratio is up 13.9% in one year

• Our median dollar/sf is up 14.4% over last year from $667/sf to $775/sf this year

• Our sales price to original list price ratio is the only indicator that isn’t up from last year, which is because it was already very high. This year, and last year, the median house is selling for 100.0% of the original list price.

The bottom line is that we have a tighter market than we had in the first half of last year. For me, these last 6 weeks have been the busiest I’ve ever been in my real estate career. With 5 out of 7 listings going to contract and a couple closed already, most got to contract in less than two week, but then the market may be changing.

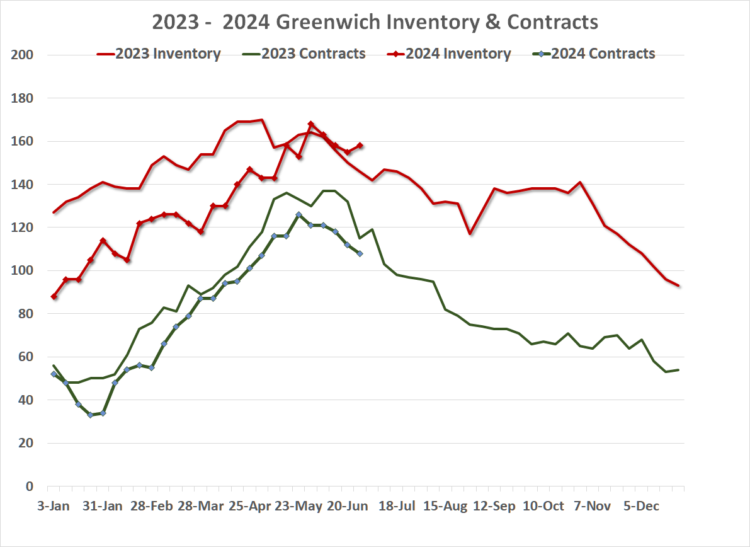

Our market saw a change in June. As noted above, our weekly inventory finally exceeded the inventory at the same time last year. It’s not a lot, but our inventory is staying above last year’s, while our contracts are dropping. Contracts normally drop in June and July as people switch into vacation mode.

The worrying sign if you are a seller is that inventory may finally be increasing in Greenwich as it has already done in much of the rest of the country. So far this year, the Bridgeport-Norwalk-Stamford MSA has been one of the top ten hottest markets in the country and Greenwich has been doing its share to make it that way.

If we get more inventory, and contracts continue to fall, we may be headed back to a more normal market, but we have a long way to go. As noted, inventory is still way down. If you just take the June sales and annualize them, you have the same or lower months of supply than if you look at sales YTD, so any movement back to a more balanced market has a ways to go, before we see anything like normal.

What we could be seeing is the bottom of the market if you are a buyer. With inventory staying steady when it normally falls and fewer contracts, we may go from combat buying to just a really tight market. The question is, is this drop just the regular summer slowdown or does it indicate something more fundamental about the market?

We do have more inventory that could come on the market, as many sellers are gridlocked. They would list their house if they had something to buy. If these frustrated sellers start listing their house, then the buyers of these houses can also list their houses. The result could be a quicker return to normalcy than others might think.

If you are a buyer, you might think that proper thing to do is to wait for this potential upcoming inventory, which can only lead to lower prices. Doing so would likely be a major mistake. Our market is so tight that it has a long way to go, before we get close to a sellers’ market.

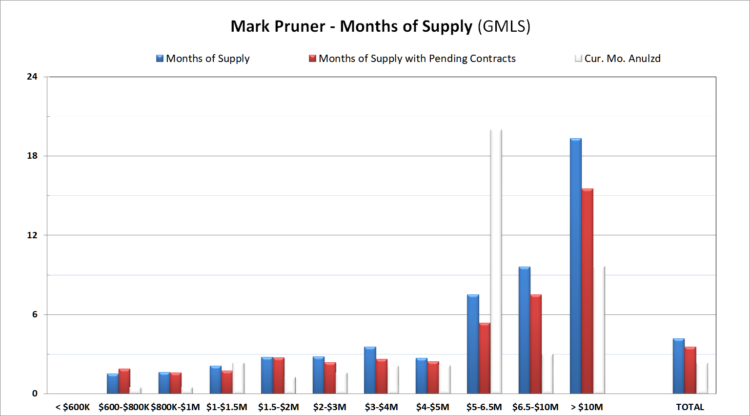

The one exception to this over $10 million where we have 29 listings and only 9 sales so far this year. Our inventory at the ultra-high-end is up 5 listings from last year, but sales are also up from 5 sales in the first half last year to 9 sales this year. Contracts are also up from 3 last year to 5 this year. So, more inventory has led to more contracts and more sales.

Also, our ultra-high-end market is a market of micro-markets. Buyers that want 10-acres for their horses are not going to buy an acre on the water and vice versa. While this is true in all price categories, as you go up in price the fragmentation of the inventory becomes greater. So yes, we have 19 months of supply over $10 million, but this is down from 28.8 months at this time last year.

For the rest of the market, we are averaging 2.4 months of supply, a true super-seller’s market. If the market really is slowing then MoS will go up, but barring a major economic issue, it’s going be awhile before we get back to anything like a normal market. Also, barring that major economic dislocation, house prices are more likely to continue to go up rather than down.

Prices may not continue to go up the 14.4% increase in price/sf that we’ve seen so far this year, but the odds of prices increasing are much greater than that they will fall or even stay flat. Buyers who wait are very likely to have to pay even more and most of our buyers aren’t using mortgages to purchase their houses, so falling interest rates may be of little value to those buyers. For buyers under $1 million, where many buyers still use mortgage financing, you have a choice of 4 houses. I

If you like a house, be ready to move, as it may be a while, before that next perfect house comes on the market.

Mark Pruner is a principal in the Greenwich Streets Team at Compass Connecticut. He can be reached at 203-817-2871 or mark.pruner@compass.com or his office at 200 Greenwich Avenue in Greenwich.