That is Until You Look Behind the Numbers

By Mark Pruner

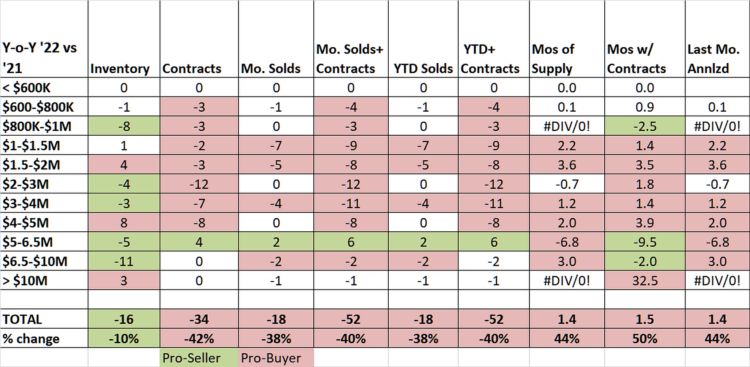

January 2023 was a horrible month for the Greenwich real estate market. Sales of single-family homes were down 38% from January 2022. The biggest drop was in what has traditionally been the bread and butter of the market; the segment from $1-2 million. In that price range, sales were down 66% from last year. Clearly, the high interest rates, which were only raised again this week, are choking off demand in price ranges under $2 million. The Fed is willing to put us into a severe recession to lower year over year inflation. At the same time, they are totally ignoring that the recent month over month inflation shows an inflation rate that is well within the Fed’s target range.

To make matters worse our contracts are down 42% from last year. Contracts are down for every price range from $600,000 to $5,000,000. Above $10 million, we have no sales and only one contract, meanwhile inventory in the ultra-luxury range has soared 15% over last year’s inventory.

Lastly, the huge drop in contracts portend a poor February which would make it the third consecutive month of below average sales. As you would expect with sales dropping like that, our months of supply has taken a 44% jump up, another indicia of cratering, if not an already cratered market.

What buyers are seeing

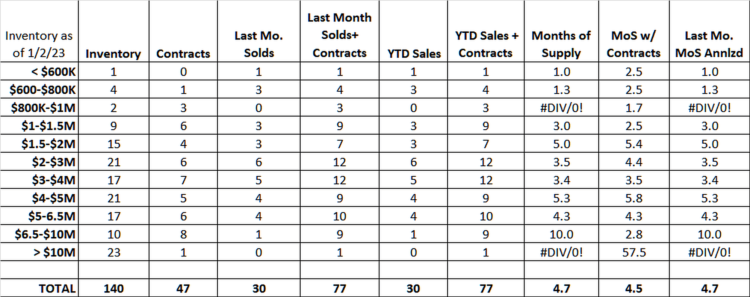

If you are buyer, however, all of these statistics, which are accurate, are not going to help you and waiting for sellers’ to dramatically drop their prices is also very likely to be a poor bet. But, why is this? The over-arching issue that makes these “disastrous” numbers not a pro-buyer’s market is our inventory has continued to stay at record low levels. We have only 140 single family home listings, when last year we had 155 listings and in January 2019, we had 476 listings.

Let’s take apart these “disastrous” numbers and see why it is still very much a pro-seller’s market.

• Sales of single-family homes were down 38% from January 2022

Sales are down from 48 sales in January 2022 to only 30 sales last month. This is a 38% percent drop, which is a pretty big decline. In hard numbers, we saw a drop of 18 sales, which looks even worse, when you see that from $1.5 – 2.0 million inventory was up 4 listings and from $4 -5 listings were up by 8 listings. Overall, we were down 16 listings from that very low inventory we had last year. Yes demand is down but supply is still nowhere close to meeting demand. This may be true even over $10 million, where we have no sales and our inventory is up as discussed below.

• The biggest drop was in what has traditionally been the bread and butter of the market; the segment from $1-2 million. In that price range, sales were down 66% from last year

From $1 – 2 million our sales have dropped from 18 sales in January 2022 to only 6 sales in January 2033. At the same time our inventory in that price range went from 19 listings to 24 listings. At this point in the year, you want to take all these with a grain of sale. We are only talking about one month’s sales and we have a lot of chatter in our numbers when you start to get this granular.

Also, if you look at the 24 listings that we have in our inventory from $1 – 2 million, you’ll see that the median days on market is 75 days and 21% have been on for over 200 days. The result is that there is not a lot of new inventory to pick from.

You can see this particularly if you look at the houses in that price range that did go to contract during this January, all of them went straight to pending. In addition, of the four contracts that were signed, 3 of the 4 contracts were on the market for less than two weeks.

Of those three, the house that I know the best is 49 Pond Place that I listed with my brother Russ. This house went public on Monday January 9th as a “Coming Soon” listing meaning that it couldn’t be shown until it went active. Three days later on Thursday, January 12th, we had a Realtor open house where 67 agents showed up, which is a great debut. Due to the Coming Soon status, we had showings lined up all Thursday afternoon right after the open house and all day Friday. On Saturday and Sunday, we held two public open houses. By Monday January 16th, 62 groups had seen the house and we had 6 offers over list in 5 days on the market. The non-contingent contract was signed on Friday, January 20th after 9 days on the market.

As you might expect a little more than half of the buyers were young family from New York City, but many of the rest were people who are renting in Greenwich as a result of Covid and are now looking to buy here. Also, we had a fair number of people looking to move out of their condos and a few folks that were looking to downsize.

The house at 49 Pond Place never made it into our inventory numbers. It went active on Thursday, 1/12 and was out of the inventory when it went to contract on Friday, 1/20. As a result you should take months of supply with a grain of salt, as the inventory doesn’t count these intra-month sales. This is also true of the other two houses. Only one of the four January sale in this price range had been listed in a prior month and hence actually appeared in inventory.

What happened with Pond Place was the right house for market put on the market, when there was little else available, as can be seen by all three of the quick sales houses. The driving factors were a newly renovated kitchen, an open adjacent family room, an expanded patio for entertaining, a good neighborhood and good schools. Right now, there are plenty of buyers that are looking for this combination, maybe not 61 other buyers, but a lot.

Sales have fallen in the $1 – 2 million price range and part of that is due to higher interest rates, but if we had anything close to the normal number of listings, we would have a lot more sales.

• To make matters worse our contracts are down 42% from last year at this time. Contracts are down for every price range from $600,000 to $5,000,000.

There is no denying that the drop in the number of contracts show a cooling market. At the lower end higher interest rates are shrinking the number of people that can buy. These higher interest rates are also leading to buyers being more picky about what they are willing to buy. Back during the “Frenzy” in the first quarter of last year, houses requiring work, even a lot of work, were flying off the market; now, not so much.

Of our 140 listings, only 20 were built in the last 3 years, then you have a gap of the 9 post-recession years to the next newest listing built in 2011. Looked at from the other end house age, 94 of the 140 listings are more than 30 years old. We actually have more houses built before 1913, than we have house built after 2019. Many of those older houses have been beautifully renovated, but they still have old bones that aren’t the first choice of today’s younger buyers and many older buyers, particularly, buyers at the higher end.

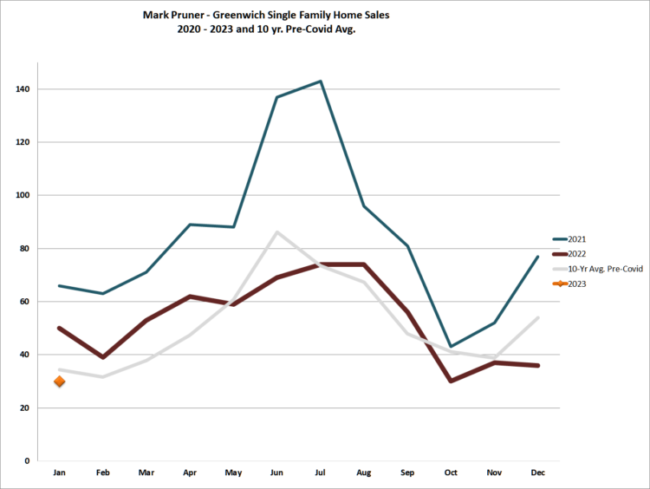

As stated above, February may be below our 10-year, pre-Covid average of 32 sales, but if we get more inventory, we might see a better month. If you are thinking about putting your house on the market, the sooner the better if it’s in good shape. If it needs some work, now is great time to do it to get ready for the spring market.

• Above $10 million, we have no sales and only one contract as inventory in the ultra-luxury range has soared 15% over last year’s inventory.

Our over $10 million market has had months of supply measured in years for all of 2022 and this January. We had only 9 sales last year, but all the rest of Fairfield County only had only 3 sales over $10 million. We only have 23 listings right now, up 3 more houses than in January 2022, so that 15% jump in inventory doesn’t seem so big when you realize it is only 3 houses.

You might think that we have only a handful of buyers at our top price ranges, but we find out this week that this is wrong. Russ and I put 76 Doubling Road on the market on Tuesday and got over a dozen showing requests in 24 hours (plus one day of Coming Soon status). We had 83 agents come through at the Tuesday open house.

It doesn’t hurt that the house is drop dead gorgeous, has a pool/guest house with a 7th bedroom, garages for 9 cars and sits on 2.53 acres in a one-acre zone with means additional FAR is available.

I expect that 2023 will be a better year for our high-end. We are seeing overseas buyers return, people being transferred in as Covid restriction fall away, and bonuses being paid. The last one comes about as many Wall Street firms spread bonuses over three years, so people may not have done so well in 2022, but a third of their bonus is from an excellent 2021 and a very good 2020 for those that got in at the bottom of the market in March of 2020.

It’s only one month, but it’s been an interesting beginning of 2023.

Mark Pruner is a Realtor with Compass. He can be reached at 203-817-2871 or mark.pruner@compass.com