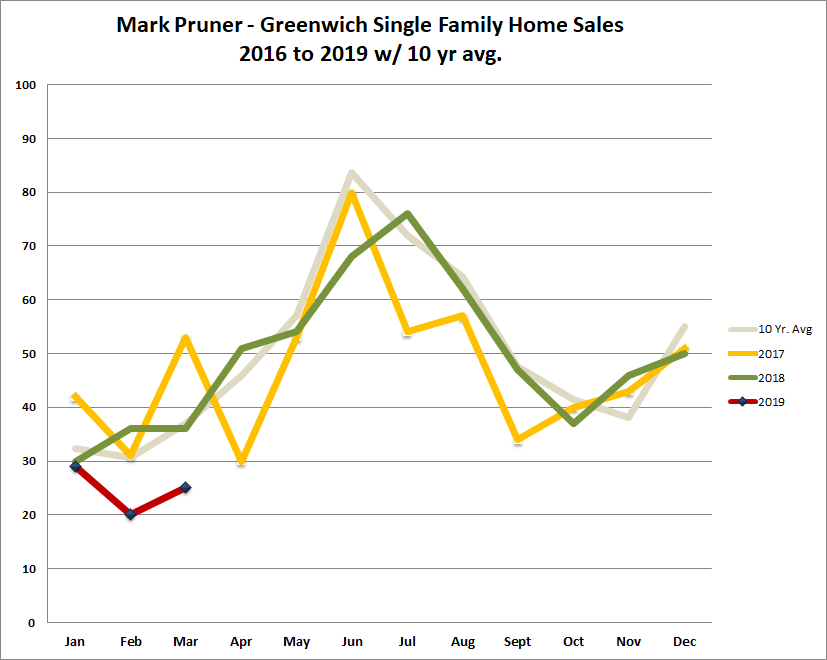

By Mark Pruner

March was a good month for deals from $2 – 3 million where we have 24 contracts waiting to close. This is up 9 contracts from last year. In addition, another 14 houses have closed in that price range. For folks in the backcountry 5 of those sales have been north of the Merritt.

We also saw sales increase in March from $3 – 4 million with 5 sales this March compared to only 2 sales in that price range in March 2018. For sellers, the market from $1 – 2 million is looking better with only 134 listings, which is down 16 listings from last year. In addition, inventory is down from $5 – 6.5 million and over $10 million by 5 houses in each case.

Now that was the good news, unfortunately, there is more not-so-good news than good news in March and the first quarter of 2019. Overall, our inventory is up 41 houses, our sales are down 28 and based on our contracts being down 39, we aren’t likely to see a significant improvement in April. When you add up the contracts and sales, we are down in every price range, excepted for the aforementioned $2 – 3 million price range.

When you look at each month in the first quarter, January 2019 sales were only down 2 sales from our 10-year average, while February sales were down 10 houses and March sales were down 11 houses from our ten-year average. As a result, our total of 74 sales for the first quarter of 2019 is down from 102 sales in the first quarter of 2018. This is a drop in overall market sales of 27% from 2018. With a 37% drop in contracts as of the end March, sales for April don’t look good at this point. The result of increased inventory and lower sales has resulted in some dramatic increases in months of supply.

For example, last year at this time we had less inventory and more sales from $4 – 5 million. As a result, we now have 99 months of supply compared to only 21 months of supply at the end of the first quarter 2018. For the entire market we have gone from 16.7 months of supply to 24.6 months of supply or from less than a year and a half to more than 2 years of supply.

When you look at the solds and contracts, the majority of our market activity is concentrated between $1 and $4 million dollars where we have 70% of our sales our 82% of our contracts. Together, we have 107 sales and contract in this mid-market range. The problem is that we have 367 listings between $1 and 4 million.

Under $1 million where our market supply is often well under the 6 months of supply level that marks the line between a buyer’s and a seller’s market, this year we are looking at a buyer’s market. Now part of that is this is the spring market with lots of new inventory coming on the market, but last year we only had 1.5 months of supply in our under $600K market and this year we have 6 months of supply in what is normally always a seller’s market.

We do have a good number of contracts between $1 and 4 million dollars and those months of supply will be coming down barring a really big surge in supply. That surge however can not be ruled out, at least between $2 and 4 million, as we already have seen 19 more listings this compared to last year in this price range.

As I said last month, it’s a good time to be a buyer, but that shouldn’t last. Interest rates are down, the stock market is up, and unemployment is low. Eventually, Hartford will defeat a whole slew of bad bills that overhang our market, and the ones they do pass will at least bring certainty to the market and let people move on with their lives. However, as Bette Davis said in “All About Eve”, “fasten your seatbelts, it’s going to be a bumpy ride” at least for one more month.