By Mark Pruner

This month is time for some slanted reporting, as it’s only fair to balance some of the Greenwich bashing reporting. In April, we had 34 sales that totaled $102,340,772. Based on a population of 62,000 people this works out to an amazing $1,650 sales for every man, woman, and child in Greenwich in just one month.

Our average sales price in April was $3,010,023. This is up a huge 25.6% from our average sales price for all of 2018, which was $2,396,448. In 2018 the median price (the price where half of the sales were above and half were below) was an enviable $1,765,000. In April of 2019, our median sales price was up even more to $2,302,000. This is a 30.4% increase in the median sales price in only 4 months.

We also had three sales over $5 million in April. The highest sales price was 33 John Street selling for $14,875,000. This property was purchased in July of 2010 for $2,875,00. The sales price represents a 517% increase in the value of the property in less than 9 years of ownership. It also shows that value of the land purchased was only 19% of the ultimate sales price, much less than the rule of thumb of land price being a third of the sales price for new development; thus, illustrating the amazing bargains to be had in backcountry land purchases.

Of the other two sales, 24 Windrose Way sold for $9,400,000 in a private sale. It is usually a sign of a hot market when properties are being sold even before they can be listed. The other sale over $5 million was 35 Winding Lane, which sold for $6,850,000. The previous purchase price less than 3 years ago was $6,000,000, for an increase of 14.2% in only 35 months.

Our 34 sales in April are up 36% from the 25 sales that we had in March of this year. May sales are expected to continue to climb with over 100 contracts waiting to close now.

The market segment from $2 – 3 million dollars is doing particularly well with 25 sales so far this year, 11 of which were in April for an increase of 3 sales over April 2018. In addition, we have an amazing 32 contracts pending in that price range, up 10 from last year.

Looking at 2019 to date in the ultra-high end (over $10 million), we have the same sales as last year, but one sale this year wasn’t reported on the GMLS. In February, 110 Field Point Circle sold for $48 million in a private sale. Were this reported on the GMLS it would be the second highest sale ever. The $48 million sale of the former Victor Borge estate, is even more impressive when you know that the purchase price was $17.5 million in 2009 in the heart of the recession and goes to show that buying when everyone else is selling and then waiting can be an excellent strategy. Taking a great property and making it even better can also lead to excellent returns. This is one of the premier properties in the U.S. and the buyer agreed.

So that’s the slanted version and everything I wrote above is completely accurate, but it actually makes me a little queasy to write it, because it’s not truly a fair representation of today’s market.

For the whole market, April was better than March, but still not that good. (April is almost always better than March as we get into the heart of the spring sales market).

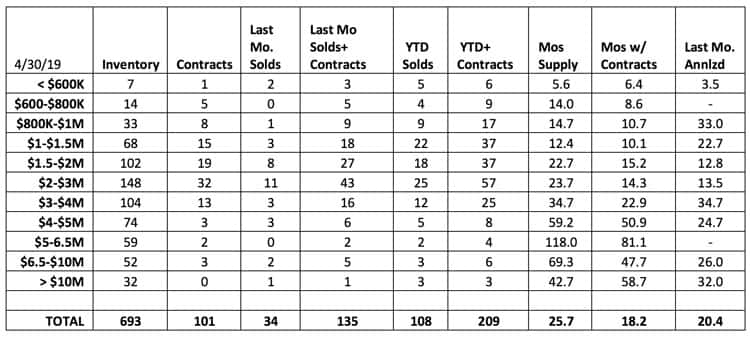

Our inventory was up 61 units or 10% to 693 single family home listings at the end of the month and is now 707 listings.

Our sales YTD are 108 or down 29% from last year. On the getting better side, there are 101 contracts waiting to close, which is down 13% from last year but better when compared to contracts being down 37% from last year at the end of March.

Our supply of homes on the market is still high, estimated to last 26 months at the present sales rate, which is up 10 months from the end of April 2018. When you factor in the contracts outstanding, we are looking at 18.2 months of supply, still higher than last year, but better.

As to changes in the average and median prices, we are seeing a greater drop in sales from $600,000 to $2 million. So, when sales are down below our average price, the average goes up and sometimes, as in April, both the average and median go up a lot. Unfortunately, the sales above $3 million are also down, just not as much as in the lower price ranges. The one exception to this is the $6.5 – 10 million price range where we had 2 sales this April compared to none in April 2018. For the year, however, we have 3 sales in this high-end category, the same as last year.

Overall, it’s still a buyer’s market and things are headed in the right direction, at least for the month of April, I think we all just wish they’d get there a lot faster.

Mark Pruner is the editor of the Real Estate pages and a regular columnist in the Greenwich Sentinel. He is also an award-winning agent with Berkshire Hathaway. He can be reached at 203-969-7900 and mark@bhhsne.com