By Patricia Chadwick

By Patricia Chadwick

Some of the greatest scandals in the world of investments have involved insider trading, which is taking advantage of significant non-public information to reap personal profits from stock transactions. Anyone who has worked in the financial industry can appreciate and understand the validity of both the letter and the spirit of the regulations surrounding inside information. In the corporate world as well, there are laws regarding the purchase and sale by members of senior management as well as the Board of Directors—all of whom are deemed by the Securities and Exchange Commission (SEC) to be perpetual insiders—that strictly limit their ability to buy and sell shares of stock in their own company.

The SEC, by being vigilant in prosecuting violators, has all but guaranteed that both investment firms and corporations will take the issue seriously. To be on the safe side of the law, some investment firms simply prohibit any and all employees—and their spouses and other immediate family members—from owning any individual stocks. The reasoning? There are more than ample other vehicles for equity investment—mutual funds, index funds, and a gallery of Exchange Traded Funds (ETFs)that can be both broadly diversified or industry focused—that don’t carry the risk of violating the law. To ensure compliance, employees in the investment business are required to have their brokerage statements automatically forwarded to their employer. Violations of the rules can result in an array of penalties, including being fired.

In the C-suite and the Boardroom, the SEC rules allow for only a specific twenty-day window in each quarter—that’s right, twenty days out of ninety—during which corporate executives and members of the Board of Directors may buy or sell the stock, and then, only after seeking and getting approval for the transaction. Even that narrow window of opportunity is liable to be shut, should there be a significant, but unannounced, event.

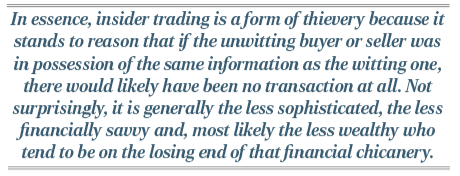

The regulations are strict but they are not difficult to comply with and importantly they are designed to create a level playing field for investors, particularly the smaller ones. The trader with “inside information” has an inequitable advantage. In essence, insider trading is a form of thievery because it stands to reason that if the unwitting buyer or seller was in possession of the same information as the witting one, there would likely have been no transaction at all. Not surprisingly, it is generally the less sophisticated, the less financially savvy and, most likely the less wealthy who tend to be on the losing end of that financial chicanery.

In 2012, President Obama signed into law a bill that was intended to apply the private sector restrictions on insider trading to members of Congress. This made sense because many Senators and Congressmen, through their committee assignments and the (often closed-door) hearings they demand of corporate managements, have access to significant and non-public information regarding industries and the companies within them.

A full decade since the passage of that regulation, it is evident that the enforcement of the law has been (might I say, deliberately) lax. It is very much a self-monitoring system, with no penalties (it seems) for delayed filings of transactions. Why isn’t there a list of prohibited investments (and perhaps even prohibited industries) that are drawn from the docket for hearings in one of the many committees and subcommittees of Congress? Why isn’t that list available online to all members of Congress, so that they can see at a glance the names of prohibited investments?

Every couple of years, there is a brouhaha in the press about the lack of transparency on the part of members of Congress regarding their own insider trading, and for a few weeks, the leadership acts as though it’s interested in resolving the issues and making some hard and fast rules. The last time that happened was about six months ago and the then Speaker of the House sounded sincere when she said they were “addressing the matter,” but then followed up with (and I may be paraphrasing a bit) something about it being a complex subject and would take some time, an obvious dodge for getting it done with any sense of urgency. Now we have a new Speaker of the House and the issue appears to have disappeared from the “to do” list of Congress as well as from the headline news. When the press puts a microphone in their face, members of Congress, from both sides of the aisle, voice platitudes about the need for regulation, but in the next breath, they spout arguments about their right to have the same opportunity as their constituents to make money in the market, as though they’d never heard of a mutual fund or an index fund, which would achieve the same objective without the possibility of violating the law.

I sometimes ask myself, “How do members of Congress find the time in their busy careers to engage in research and analysis on stocks for their personal portfolios?” When I was a stock analyst, it was more than a full-time job, and I never had the luxury of dabbling in legal matters, or other unrelated past times.

The bottom line of this column is to bring home the point that rules, regulations and laws that apply to regular citizens ought to apply as well to those who serve us in the Government—federal, state, municipal and local.

{kind=link}