By Mark Pruner

By Mark Pruner

Increasing interest rates have been good for the Greenwich real estate market, the falling financial markets have not. The increase in interest rates has led to stories about the slowing real estate market nationwide, which has prompted more people to list their houses giving our surplus of buyers something to bid on.

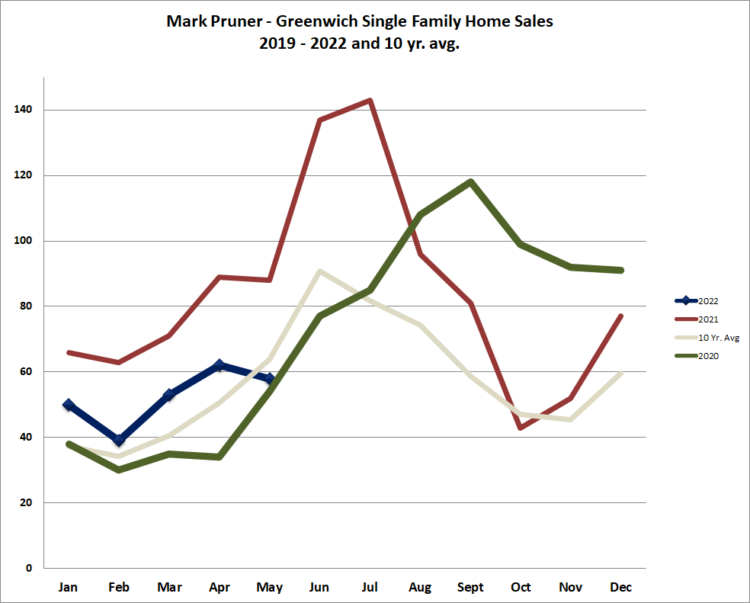

If you are looking for slowing, you can certainly point to the unusual drop in sales from April to May this year. In April 2022, we had 62 sales of single-family homes. Last month in May we only had 58 sales reported so far or a drop of four sales. This is below our 10-year average for May of 64 sales and only the 2nd time we’ve seen sales below average in the last 23 months.

However, you only have to go back to last May to see a similar pattern. In May 2021, we saw sales drop from 89 sales in April 2021 to 88 sales in May. Sales then took off, and the next two months were all-time record months for sales. We won’t be setting any all-time records this June. Last year at this time, we had 265 contracts waiting to close and this year we only have 155 contracts. I wouldn’t be too worried, however as this is 44% more contracts, than we had in our last pre-Covid year of 2019. Also, we have those 155 contract, when our inventory of homes is down 45% from last year. Buyers are still moving quickly on what listings come on the market.

This 45% drop in inventory is a big change from last year, but it is a huge change from prior years. In 2019, we had 738 listings on June 1, 2019, i.e., we are down 76% in inventory from our last pre-Covid year.

The good news for buyers is that the rise in interest rates has gotten the attention of a couple of dozen Greenwich homeowners who listed their houses faster than buyers could reduce the inventory. We started the month with 170 house listings on the GMLS and ended it with 179 listings for a small increase. These monthly figures hide a significant intra-month drop from 2022 inventory peak in the third week of May of 189 home listings. This peak lasted for a day only to sink to 179 listings by the end of the month. Net for the month we picked up only 9 listings due to very active buyers.

Contracts were similar starting the month at 152 contracts and ending up with a tiny rise to 155 contracts. That tiny rise, however, was significant on both the upside and the downside. Normally, you’d expect a significant rise in contracts in May as deals get done in May before leading to our biggest sales months in June and July, as these deals close. No significant contract rise indicates a noticeable slowing in the market.

On the flip side however, we still have a very active market compared to the aforementioned, 108 contract in May of 2019. Russ and I had 4 of our buyers go to multiple bids in the last two weeks of May. It is still a hot market, all the way up to $5 million. There is zero inventory below $600,000 and from $4 to 5 million, we have 12 listings with 49 sales and contracts meaning we are looking at only 1.6 months of supply. The market from $3 – 4 million is even tighter with just 1.4 months of supply. Annualize, May sales indicate the price range from $3 – 5 million is likely to get hotter.

We have plenty of buyers under $5 million, so that market will continue to be busy; just slightly less busy than before. Markets are driven by emotion and all the stories out there are of markets that are slowing precipitously. In Greenwich, so far it just isn’t so. If you compare the April 2022 market to the May market you see a slight, but scattered tick up in inventory, while contracts and monthly sales are essentially unchanged. Overall, the market went from 3.3 months of supply in April to 3.4 months of supply in May. Until we get lots more inventory, we are going to continue to have a tight market.

Now, this doesn’t mean that the shrewd buyer can’t cut a better deal for themselves in June than they could in March when inventory hit an all-time low of 136 listings. Other buyers are moving slower and making lower offers. Higher interest rates are making some people think twice and some sellers want to sell before the market is going to “crater”. Knowing this, the prepared buyer can make deals, with motivated sellers, that weren’t there to be made before. Buyers still need to move quickly; they just have a somewhat better chance of succeeding on some properties.

What would it take just to get buyers back to a balanced market with around 6 months of supply? If we were to keep our current inventory level of 179 home listings for the rest of the year, you’d actually have to have negative sales inf 5 of our 10 price ranges to get to 6 months of supply at year-end. Our total sales would have to drop to 358 sales for the entire year to get to a balanced market. This number is even lower than the 370 sale we had in 2009 the worst year of the Great Recession, so, not very likely.

How about keeping the sales rate the same for the rest of the year and increasing inventory? This would mean total sales for the year of 629 sales, almost the same as out ten-year average. That seems reasonable, but we would have to end the year with 1,258 listings to reach 6 months of supply. This means 1,079 new listings also very unlikely.

If we double our present inventory and reduce our sales rate to 75% of what it has been for the first 5 months, we actually overshot and get 9.1 months compared to our present 3.4 months of supply. We would end up selling only 210 houses in the last 7 months compared to 262 sales in the first four months and finish in a good buyer’s market.

Is that possible, yes, but the Fed would really have to overdo the interest rate increases (which they have done before). Jamie Dimon and Elon Musk and other traditional managers would have to kill off the work from home buyers’ movement and the financial market would need to stay down or go lower possibly with an assist from international issues.

To actually get to 6 months of supply, we could increase our inventory by 50% and lower our sales rate by 15%, to get 270 listings and 534 sales at year-end. A little better than 2019, but not a lot. Maybe, putting your house on now, might not be such a bad idea.

In general what this shows is that our inventory is so low, that months of supply is very sensitive to changes in inventory. On a percentage basis these changes are huge, but inventory would still only be a fraction of historical norms.

Stay tuned, it’s going to be an even more interesting rest of the year.

Mark Pruner is a realtor with Compass Connecticut. He can be reached at 203-969-7900 or by email at mark.pruner@compass.com

{kind=link}